JIIA Strategic Comments (2026-13) The Economic Impacts of the Japan-MERCOSUR EPA

Papers in the "JIIA Strategic Commentary Series" are prepared mainly by JIIA research fellows to provide comments and policy-oriented analyses of significant international affairs issues in a readily comprehensible and timely manner.

Economic and trade developments have given rise to uncertainties globally. Oil price surges, turmoil in international financial markets and other adverse impacts have become growing concerns as Russia’s military invasion of Ukraine has continued, the United States (US) and Israel have attacked Iran, and economies worldwide have been forced to respond to additional tariff measures imposed by US President Donald Trump. On the other hand, steady progress has been made in trade and investment liberalization/facilitation efforts through regional free trade agreements (FTAs) and economic partnership agreements (EPAs) under the multilateral free trade system overseen by the World Trade Organization (WTO). After the US withdrew from the Trans-Pacific Partnership (TPP) Agreement in 2017, the United Kingdom (UK) joined the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) in 2024, which entered into force in 11 countries (Australia, New Zealand, Japan, Brunei, Malaysia, Singapore, Viet Nam, Canada, Mexico, Chile and Peru) without the US in 2018. Several economies – including China, Chinese Taipei, Cambodia, Indonesia, the Philippines, Costa Rica, Ecuador, Uruguay, Ukraine and the United Arab Emirates (UAE) – have since formally applied for CPTPP membership, and accession procedures for Costa Rica and Uruguay have been negotiated. Meanwhile, the CPTPP took part in ministerial conferences on trade and investment with the Association of Southeast Asian Nations (ASEAN) and the European Union (EU) in November 2025.

Economies across the world engaged in international trade tend to skew heavily toward commerce with neighboring countries. Most FTAs and EPAs have been intra-continental, with inter-continental FTAs and EPAs such as those between Asia and America being far less common. Since the Regional Comprehensive Economic Partnership (RCEP) Agreement entered into force in 2022, Japan has signed a Japan-Bangladesh EPA (February 2026) and is now party to 22 FTAs/EPAs and related initiatives that have been signed and entered into force.1 That said, the only agreements it has concluded with non-CPTPP Western countries have been those with Switzerland, the EU and the US. It should be noted that neither the RCEP Agreement nor the US-Japan Trade Agreement (USJTA) have not been included in the WTO’s Regional Trade Agreement (RTA) Database. Tariffs have not been reduced on “substantially all the trade” as required to be deemed a free trade area under the General Agreement on Tariffs and Trade (GATT). Considerable room remains for further tariff reductions among Japan, the US and China.

The Mercado Común del Sur (MERCOSUR) is a South American common market, the customs union for which was established in 1995 for the purpose of removing tariffs and other trade measures within the region. Seven countries (Chile, Colombia, Ecuador, Guyana, Panama, Peru and Suriname) have become associate states alongside the six full-member states (Argentina, Bolivia, Brazil, Paraguay, Uruguay and Venezuela). The total GDP of these 13 countries amounted to US$4.7 trillion in 2025, exceeding Japan’s (US$4.4 trillion).2 Brazil’s GDP, the 11th largest in the world, accounts for around 50% of MERCOSUR’s GDP, followed by Argentina’s, Colombia’s, Chile’s and Peru’s. These five countries together make up close to 90% of MERCOSUR’s GDP.

MERCOSUR holds a 1.32% share in Japan’s export market and a 2.83% share of Japan’s imports3, smaller than the share MERCOSUR – even including the CTCPP members Chile and Peru – holds in world economy, as shown in Table 1. By industry, Japan mainly exports motor vehicles and parts (40.3%), electronic products (22.6%) and other machinery and equipment (6.9%) to MERCOSUR, altogether accounting for around 70% of Japan’s exports to MERCOSUR; notably, the percentage of motor vehicles and parts exports is nearly double that of such exports to the world as a whole. Meanwhile, Japan imports mining products (52.0%) and agricultural, forestry, fishery and food products (32.1%) from MERCOSUR, which combined exceed 80% of Japan’s imports from MERCOSUR and twice the share of such imports from across the globe. While Japan does import beef from Argentina, Brazil and Chile, these imports from MERCOSUR constitute less than 1% of Japan’s total beef imports; Australia and the US together account for more than 80% of Japan’s beef imports. It should be noted that the average tariff rate imposed on Japan’s imports from MERCOSUR is 1.9%, not so different from its global average (2.1%). On the other hand, the average tariff rate imposed on MERCOSUR imports from Japan is 9.6%, more than twice its world average (4.2%). By industry, Japan continues to place import tariffs on agricultural, forestry, fishery and food products as well as textiles and apparel, while MERCOSUR maintains high tariffs across all industries – especially motor vehicles and parts – apart from mining.

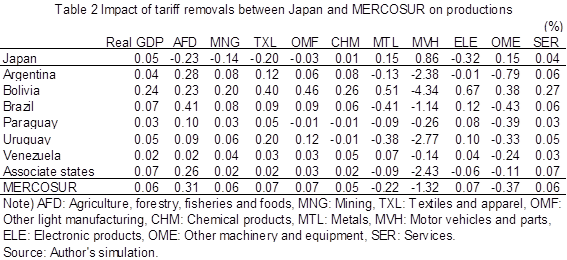

Simulation analysis using the GTAP-provided standard computable general equilibrium (CGE) model of global trade shows that if Japan and MERCOSUR were to conclude an EPA and mutually remove 100% of tariffs, Japan’s real GDP would increase by 0.05% and MERCOSUR’s by 0.06%, with both economies enjoying macroeconomic benefits of similar magnitude, as shown in Table 2. Japan’s exports to MERCOSUR would increase by 82.6%, nearly doubling, boosting its global exports by 0.25%. At the same time, lifting tariffs on imports from MERCOSUR would only increase Japan’s inflow from that bloc by 9.9% because non-tariffed mining commodities constitute half of these imports, while its total imports on a global basis would move up by 0.38%. Declining import prices would also lead to greater private consumption. Model analysis shows that real GDP gains on both sides would primarily be driven by MERCOSUR’s removal of tariffs on imports from Japan rather than Japan’s abolition of tariffs on imports from MERCOSUR. The key to making an economic impact would thus be tariff reductions by MERCOSUR, which has imposed higher tariffs than Japan as discussed above. It should be noted here that Japan’s real GDP would increase by an estimated 0.09% if tariffs between Japan and the US were to be eliminated. Given that Japan’s exports to MERCOSUR are less than a tenth of its exports to the US, the fact that the real GDP impact of mutual tariff removals with MERCOSUR would be around half of that from tariff removals with the US seems relatively large.

The economic impacts of tariff removals would be larger at the industry level than at the macro level discussed above. Trade theory posits that winners and losers would emerge, reflecting the comparative advantages of economies. That said, the effects in practice would be affected by the tariff levels prior to removal. It would be useful for policy makers to study this issue quantitatively using economic models, which serve as laboratories for the social sciences. The simulations in this article suggest that Japan’s motor vehicles and parts production, on which MERCOSUR applies the highest tariffs, would see a larger increase (0.86%) than other industries, and that the production of other machinery and equipment – but not necessarily of electronic products – would also rise. On the other hand, the production of agricultural, forestry, fishery and food products as well as of textiles and apparel, commodities that remain subject to Japanese tariffs, are shown as declining because of a tariff removal-driven expansion of imports. The drop in agricultural, forestry, fishery and food products production (-0.23%) would only be a tenth of that stemming from the elimination of tariffs between Japan and the US (-2.37%), so in-depth analysis of sensitive and other relevant sectors should be conducted to more reliably assess the actual economic impacts. In contrast to Japan, MERCOSUR’s production of agricultural, forestry, fishery and food products as well as of textiles and apparel would likely climb, while that of motor vehicles and parts as well as other machinery and equipment would drop, with the magnitudes of these changes varying from country to country.

EPAs have been expected to cover a wide range of trade policy measures, including non-tariff measure (NTM) reductions and service and investment liberalization. As pointed out by Ciuriak, Dadkhah and Xiao (2016)4, though, NTM reductions based on agreements actually concluded under the TPP – termed a new 21st-century-style EPA that comprises 30 chapters covering such matters as NTMs, services, finance, investment, telecommunications, e-commerce, government procurement, competition policy, intellectual property, labor and the environment alongside tariffs – would have a limited impact vis-à-vis the more substantial effect of tariff reductions. Ideas have been proposed for rebuilding a rule-based international economic order, but more essential from the perspective of economic impact are policy measures that would specifically affect the prices and volumes of trade in terms of monetary value as well as trade policy predictability and stability. Japan’s EPAs also appear to have given due consideration to development through economic cooperation, in contrast to its FTAs that have focused on trade liberalization. As an EPA with MERCOSUR would likely help cut MERCOSUR’s tariffs significantly, Japan’s contributions in other areas could be expected to generate two-way economic benefits.

- Economic Partnership Agreement (EPA) / Free Trade Agreement (FTA) and Related Initiatives, Ministry of Foreign Affairs of Japan, April 10, 2026.

https://www.mofa.go.jp/policy/economy/fta/ - World Economic Outlook (WEO) Database, International Monetary Fund (IMF).

https://www.imf.org/en/publications/sprolls/world-economic-outlook-databases - GTAP 11 Data Base, Global Trade Analysis Project (GTAP).

https://www.gtap.agecon.purdue.edu/databases/v11/ - Ciuriak, Dan, Ali Dadkhah and Jingliang Xiao (2016), “Better In than Out? Canada and the Trans-Pacific Partnership,” E-Brief, C.D. Howe Institute, April 21, 2016.